When you apply for a Personal Loan, one of the most important things to understand is your Equated Monthly Instalment (EMI). Your EMI determines how much you will repay every month and directly affects your cash flow, savings and overall financial stability.

Many borrowers focus only on loan approval and ignore EMI planning. However, calculating EMI properly before borrowing helps you avoid repayment stress and manage finances better.

In this guide, we will explore different methods to calculate your EMI and understand how the Personal Loan interest rate affects your repayment.

What Is Personal Loan EMI?

EMI is the fixed monthly amount you pay towards repaying your Personal Loan. It consists of:

- Principal repayment

- Interest component

In the early months, a larger portion of EMI goes towards interest. Over time, the principal repayment portion increases.

Understanding this structure is important before calculating your EMI.

Method 1: Using the Standard EMI Formula

The EMI is calculated using a standard mathematical formula:

EMI = P × R × (1 + R)^N ÷ ((1 + R)^N − 1)

Where:

- P = Principal loan amount

- R = Monthly interest rate

- N = Loan tenure in months

Example

Suppose:

- Loan amount: ₹3,00,000

- Interest rate: 12% per annum

- Tenure: 3 years, which is 36 months

First convert annual interest rate into monthly rate:

12% ÷ 12 = 1% per month

So R = 0.01

Now plug values into the formula. The calculation gives you the EMI amount.

While the formula provides accuracy, manual calculation can be complex. It is useful for understanding the concept but not practical for everyday use.

Method 2: Using a Personal Loan Calculator

The easiest way to calculate EMI is by using an online calculator.

A digital EMI calculator allows you to:

- Enter loan amount

- Enter tenure

- Enter estimated Personal Loan interest rate

- Instantly view EMI

- See total interest payable

This method is quick, accurate and practical.

Digitally focused banks in India, such as ICICI Bank, provide structured digital tools that allow borrowers to calculate EMI before applying. Using these calculators helps you compare different tenure and rate combinations.

How Personal Loan Interest Rate Impacts EMI

The Personal Loan interest rate plays a crucial role in determining EMI.

Even a small change in rate can significantly impact:

- Monthly EMI

- Total interest payable

- Overall repayment amount

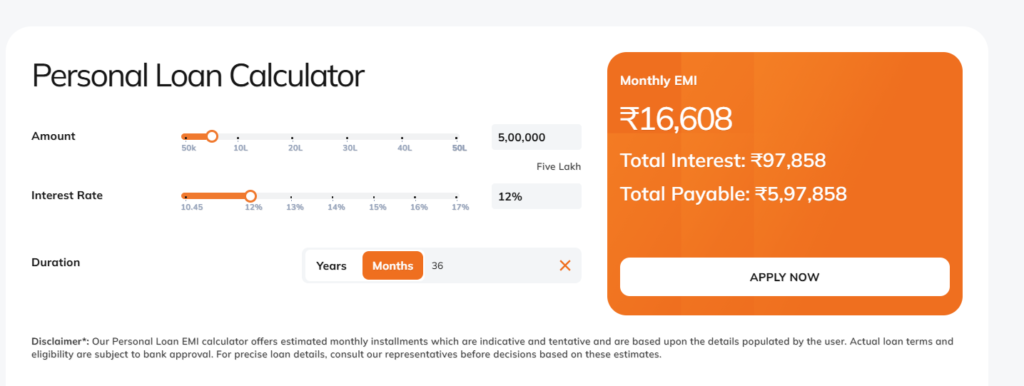

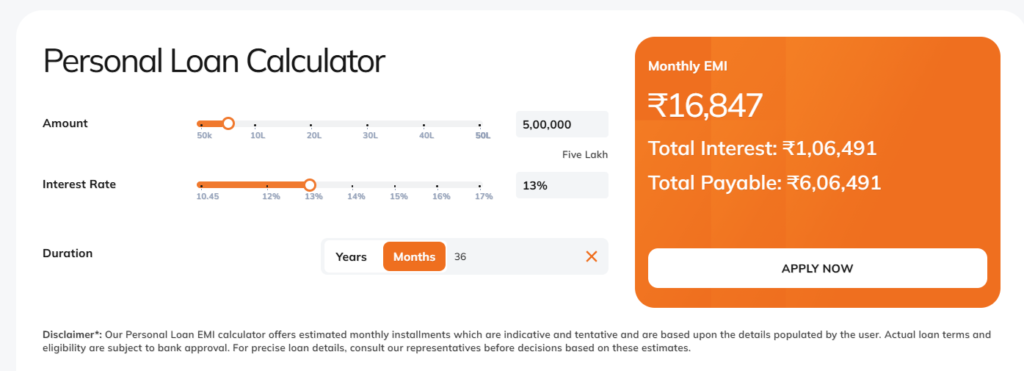

Example of 1% Difference

Consider a ₹5,00,000 Personal Loan for 36 months.

At 12% interest rate, your EMI will be ₹16,608 and total interest would be ₹97,858.

At 13% interest rate,your EMI will be ₹16,847and total interest would be ₹1,06,491.

The difference in the total interest paid over the tenure will be ₹8,633.

That 1% increase can lead to:

- A higher monthly EMI outgo

- A noticeable rise in the total repayment amount

Even a small change in interest rate can have a measurable impact on your overall loan cost. This is why comparing interest rates before finalising your loan is essential.

Choosing the Right Tenure

Your loan tenure plays an important role in determining your EMI and overall repayment cost. A shorter tenure results in a higher EMI, but it reduces the total interest payable and helps you close the loan faster. On the other hand, a longer tenure lowers your monthly EMI, making repayment more manageable, but it increases the total interest paid and extends the repayment period.

If your priority is to reduce your monthly financial commitment, a longer tenure may be suitable. However, if your goal is to minimise the total interest cost, opting for a shorter tenure can be beneficial. It is advisable to use an EMI calculator to compare both options before making a decision.

How to Plan EMI Comfortably

When calculating your EMI, ensure that it does not exceed 40 to 50 per cent of your monthly income. It is equally important to maintain adequate emergency savings, factor in any existing EMIs and assess your job stability before committing to a loan. Borrowing within comfortable limits helps you manage repayments smoothly and reduces the risk of financial stress.

Fixed EMI vs Reducing Balance

Personal Loans in India are usually offered on a reducing balance method. This means:

- Interest is calculated on outstanding principal

- Interest portion reduces over time

This is beneficial compared to flat rate calculation where interest is charged on full principal throughout the tenure. Understanding the type of rate calculation helps you assess actual cost.

Additional Factors Affecting EMI

Besides interest rate and tenure, EMI may also be influenced by:

- Processing fees

- Insurance premiums

- Prepayment charges

- Late payment penalties

While these do not directly change EMI calculation formula, they affect total loan cost.

Always review loan agreement carefully.

When Should You Recalculate EMI?

You should recalculate EMI if:

- Interest rate changes

- You plan partial prepayment

- You want to change tenure

- You are considering balance transfer

Recalculation helps you understand savings potential.

Many borrowers use structured digital banking tools to simulate these changes before making decisions.

Why EMI Planning Is Important

Calculating your EMI in advance gives you better financial clarity and helps you make informed borrowing decisions. It allows you to:

- Avoid over-borrowing by understanding exactly how much you can comfortably repay each month

- Maintain financial stability by aligning your EMI with your income and existing commitments

- Plan investments simultaneously without disrupting long-term financial goals

- Protect your credit score by ensuring timely repayments

Missing EMIs can negatively impact your credit history and may affect your future borrowing ability. A disciplined repayment strategy supports smoother and more sustainable financial growth.

Smart Borrowing Tips

Before applying for a Personal Loan:

- Compare interest rates

- Use EMI calculator for different scenarios

- Choose shortest comfortable tenure

- Maintain strong credit score

- Avoid borrowing maximum eligible amount unless necessary

Leading banks such as ICICI Bank offer digital loan facilities that allow borrowers to check eligibility, view customised loan offers and evaluate EMI options before confirming the loan. Using such tools ensures informed decisions.

Final Thoughts

Calculating your EMI is not merely a technical step; it forms the foundation of responsible borrowing. It helps you understand your repayment commitment clearly before taking a loan.

You can calculate EMI using a standard formula, through approximate estimation or by using an online calculator. Among these, an EMI calculator is the most reliable and convenient option, as it provides quick and accurate results.

Before applying, carefully assess how the Personal Loan interest rate and tenure will affect your monthly outgo and total repayment. A well-planned Personal Loan can support your financial goals without disturbing your monthly stability. Thoughtful EMI calculation today can help ensure smoother and more stress-free repayment in the future.